My account

My account

The scoring system, based on the data of the largest database of credit history bureaus in Ukraine, allows you to simplify and accelerate the credit decision making process, and ensures the maximum efficiency in risk prediction.

The study and analysis of a credit history, by a credit expert, especially if it includes a large number of contracts, takes a much time and has low efficiency.

Automation of the assessment of credit history status, using a scoring model, allows you to carry out such an analysis in a matter of seconds, taking into account the influence of various aspects and their combinations, based on statistical regularities.

When developing a scoring model, a set of so-called «predictors» is formed – factors that, hypothetically, can influence the further credit behavior of the borrower. These predictors are then tested on large volumes of data. Actual impact and significance of each predictor are determined. This is how a scoring model is built.

The result of the scoring model work, is a credit score – a numerical indicator assessing the likelihood of a borrower’s default, based on his/her credit history data.

Credit Score Report is intended for obtaining the credit scores of individuals and entrepreneurs. To obtain credit scores for legal entities, use the SME Scoring service.

borrower’s current ID data and the history of changes made to it.

digital assessment of the creditworthiness of the subject based on the data from the borrower’s credit history. Shows the probability of default.

parties to enforcement proceedings; information about the contractor (name, contacts); characteristic of enforcement proceedings (status, type, opening date); history of changes in enforcement proceedings.

search results in the list of lost and invalid documents.

assessment of the probability of late payments on a short-term loan from a microfinance institution.

real-time information about the number of requests on the subject.

сomments from the subject, reports of a lost passport, disputing a loan contract or activated FREEZE, credit history correction, certificate of passing the financial literacy test and information about the possible death of the person.

Information about a business entity in respect of which bankruptcy proceedings are ongoing or have been completed.

- improving the efficiency of credit risk assessment;

- automation of credit risk assessment;

- simplification and acceleration of credit decisions;

- elimination of the human factor.

- acceleration of credit application processing, increases business performance and client loyalty,

- predicting a borrower’s behavior allows you to estimate risks and manage characteristics of credit products, to ensure optimal performance and maximum efficiency,

- determination of the optimal target audience, allows you to attract the desired customers more effectively,

- timely identification of borrowers, with a high likelihood of default, allows you to minimize the portfolio of bad loans.

After the Agreement-Application has been signed, and login and password have been obtained, a report can be requested through:

https://secure.ubki.ua:4040/b2_api_xml/ubki/xml

Requesting a report is possible only subject to the individual’s consent

Frequently Asked Questions

Credit scoring is a system of assessment of creditworthiness (default risks), based on numerous statistical models.

The model includes more than 200 predictors, derived from credit history data and its relationships. For example, the presence of current and past overdue payments, the number of outstanding and paid-off loans, their amounts and duration, the frequency of requests for credit history, in order to approve loans, etc.

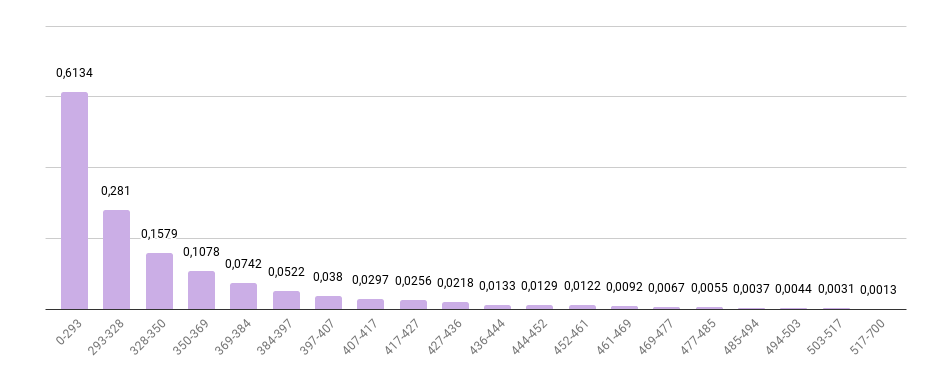

The credit score value, obtained as a result of credit scoring for individuals, ranges from 0 to 700, and directly corresponds to the level of creditworthiness.

It means, the higher the credit score value, the higher the likelihood that the borrower will fulfill his or her credit obligations in good faith. If there is a current overdue payment, for a period of more than 90 days in the borrower’s credit history, the credit score will be 0.

The range from 0 to 700 is divided into subranges:

0-250 – very low

250-350 – low

350-450 – medium

450-550 – high

550-700 – very high

- If a borrower does not have the credit history, or it is not informative (very short-term or includes only credit card agreements without credit tranches), the credit score is not calculated, due to insufficient data.

- If a borrower has applied to the bureau to dispute some data in the credit history, and the procedure is still on-going, the credit score is not calculated, to prevent potentially erroneous scores.

In addition to basic credit scoring for individuals, it will be useful to utilize the additional scoring products for specific purposes.

- Short-term loans have their own specifics and target audience. For microfinance organizations, we have developed a highly specialized model, that allows them to predict risks for their products more accurately – MFI scoring.

- In the absence of a credit history, it might be useful to utilize alternative scoring models, in particular, a model based on data on the use of a Visa card (amount and categories of expenses, payment patterns and their stability, rejected transactions) – Visa Transaction Underwriting Score.

- The more accurately, that the target function and the training set for building a scoring model correspond to the realities of your business, the more effective the risk assessment will be. The bureau can create an Individual scoring for your specific target function and sampling parameters.

Apply for cooperation