My account

My account

Identifying high-risk loan applications, in order to protect companies from fraud

The service is based on comparing the corresponding data from a request, with that of historical application data in the Bureau’s database. Fraud rules allow us to detect logical inconsistencies and previously compromised data. You can use the rules that have already been implemented in the UBCH, or you can create your own rules with a rule constructor.

Antifraud verification allows for detecting high-risk indications in loan applications, ensuring protection from fraud.

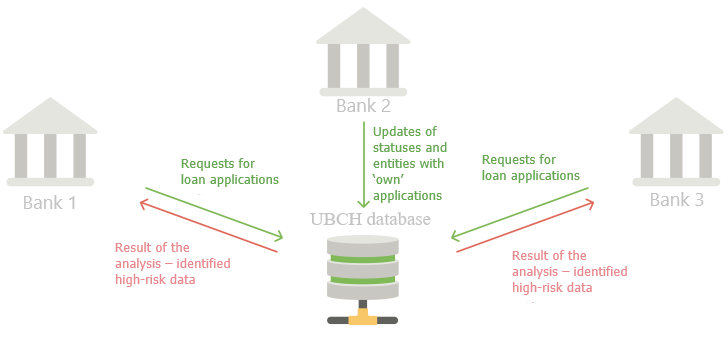

- When a borrower applies for a loan, the Partner forms an application with the borrower’s dossier data, and submits a request to the service;

- data is recorded in the database, and compared with historical applications for the same person, from all the partners of the Bureau;

- the Partner receives a report on the results of the Antifraud verification;

- the Partner conducts additional checks via their internal procedures, and makes a decision on the application;

- the Partner transmits the information about the decision on the application and data about the detected fraud, if any;

- data on the result of the application is recorded in the Bureau’s database, to account for subsequent checks.

The service outlines potentially risky applications, on the basis of the following activities:

- validation of application data by internal comparison of the data, specified in the current application, with other data;

- comparison of new applications data, with all the applications stored in the database, and previously transferred and updated by UBCH Partners;

- search for logical discrepancies and matches with other applications;

- identifying applicants with confirmed risky events.

The scoring model of the UBCH antifraud system represents the total points for all the rules activated in the application being examined. The calculation result for the application can be separated into two zones: a black zone (score >=432) and a gray zone (score of less than 432). The black zone is a prerequisite to making a decision automatically by the Partner. The gray zone requires additional checks from the Partner’s side.

To ensure full functions of the service, 2 requests must be made:

- the first one is required to transfer the application, and receive the response from the UBCH;

- the second one is needed to update metadata of the information about the decision on the application.

This is important to ensure effective operation of the interbank antifraud monitoring system, based on application data.

Service Hit Rate > 80%

Based on the report and your verification procedures, you can make a decision on the application. The application status is transmitted to the service by the second request, and it will be taken into account in the subsequent checks.

https://secure.ubki.ua:4040/b2_api_xml/ubki/xml

Apply for cooperation